New Mansion Tax Rates:

Governor Andrew Cuomo and the New York State Legislature just adopted the Fiscal Year 2020 (April 2019 through March 2020) budget. The spending plan for the upcoming fiscal year addresses critical issues that impact our industry. The Real Estate Board of New York was engaged on these issues throughout the budget process and we are currently assessing our state legislative priorities as the session continues throughout the month of June.

TRANSFER AND MANSION TAX RATES

As a result of the State budget just adopted in Albany, hundreds of millions of dollars on an annual basis will flow from the City’s real estate sector toward supporting the region’s mass transit network. The Governor and Legislature agreed to make changes to the New York State Transfer Tax and the Mansion Tax to raise revenue.

1) A new New York State Transfer Tax Rate of 0.65% applies the following:

- Residential 1-3 Family, condo, and co-op sales for $3 million or more

- Commercial sales for $2 million or more

All other sales remain at the old rate of 0.40%.

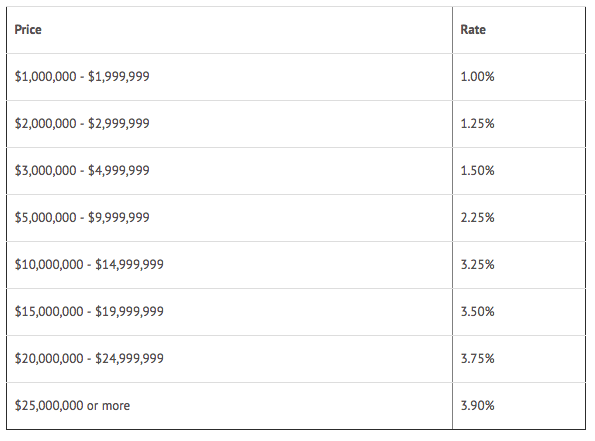

2) New Mansion Tax rates

Instead of a 1% tax on sales of $1 million or more, the new rate increases based on the sales price.

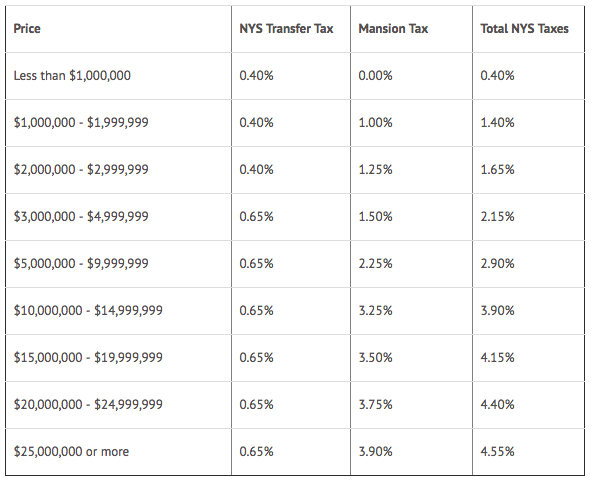

The table below shows the new total Mansion and New York State Transfer Taxes paid by 1-3 family homes, condos, and co-ops:

Effective Date: These tax changes take effect July 1, 2019, and shall apply to conveyances occurring on or after such date other than conveyances which are made pursuant to binding written contracts entered into on or before April 1, 2019, provided that the date of execution of such contract is confirmed by independent evidence, such as the recording of the contract, payment of a deposit or other facts and circumstances as determined by the commissioner of taxation and finance.

These tax changes will result in a substantial outflow of resources from the real estate sector to the region's mass transit network. It is critical to monitor the impact these tax changes and other tax and policy changes on the federal, state and city level will have on investment, job creation, and property tax revenue generation in New York City moving forward. With that said, we are appreciative that State leaders did not move forward with a misguided recurring pied-a-terre tax that was not well-thought out and had the potential to have significant adverse impacts on job creation and property tax revenues.

CONGESTION PRICING

The inclusion of congestion pricing is a monumental step forward for New York City that will allow our economy to continue to grow and thrive. Congestion pricing will generate billions of dollars to modernize our transit infrastructure, reduce the crushing burden of traffic congestion in Manhattan and provide environmental benefits. It is now critically important that such funds generated by congestion pricing and the changes made to the Mansion Tax and New York State Transfer Tax be utilized in the most effective manner possible, producing a twenty-first century mass transit system that a global city like New York deserves.

PREVAILING WAGE

The adopted State budget did not include provisions that would have significantly expanded the application of prevailing wage standards for construction and building service workers. As written, these proposed changes would have dramatically increased costs for numerous projects that are integral to our City and State economy. More time is needed to allow for a more thoughtful approach. As the organization whose members are the predominant employers of unionized building service workers and construction trades, we will continue to work with these labor unions to advocate for policies that promote good wages while being mindful of the need to create jobs and promote economic development and affordable housing.

Peter Ashe Real Estate is committed to the Fair Housing Act under the New York State Human Rights Law. To learn more about it, please click here.

Peter Ashe Real Estate is committed to the Fair Housing Act under the New York State Human Rights Law. To learn more about it, please click here.